|

March 1966 Popular Electronics

Table of Contents

Table of Contents

Wax nostalgic about and learn from the history of early electronics. See articles

from

Popular Electronics,

published October 1954 - April 1985. All copyrights are hereby acknowledged.

|

Note: The tax-related information

presented in this 1966 Popular Electronics article is almost certainly outdated and invalid.

My purpose for posting it is to provide some insight into potential tax advantages available

to anyone engaging in a small business. The IRS provides multiple classifications for

businesses, including the simplest, Sole Proprietor, where essentially you report your

business gains and losses as part of your personal income tax filings. The next step

up is a Limited Liability entity where some formal paperwork is filed to isolate personal

liability from business liability. From there you can incorporate and have the company

be a stand-alone taxable entity that pays its employees. Each has unique advantages and

disadvantages, but all permit you to deduct qualified expenses from your reportable income.

Even though RF cafe is a sole proprietorship, I am allowed to deduct part of my Internet

and phone subscriber services, monthly ISP hosting services, car mileage for business-related

travel, part of computer and software costs, etc. I could deduct part of my home and

utilities costs but don't for a couple reasons. First, in order to do so you must have

a permanently sanctioned area set off specifically for the office. Second, if I ever

move from the house or eliminate the office area, all of the previous deductions must

be given back. Third, according to what I've read the IRS tends to audit more often in-home

businesses that claim office space. RF Cafe's (and our personal) finances are tracked

in

Quicken Home & Business.

TurboTax Home & Business is used for state and federal filings.

Being a sole proprietorship keeps things very simple.

Electronics Moonlighters

By Ken Kirkpatrick By Ken Kirkpatrick

Did you build, repair or service electronic gear in 1965? If so, take advantage of

tax savings

Although few Americans feel so strongly about the income tax that they don't want

to pay it, the U.S. Government doesn't want them to overpay, or to neglect to take deductions

they are legally entitled to take. Most electronics enthusiasts are unaware that the

Government might consider them "moonlighters" - one of several thousand Americans who

operate profitable spare time hobby-businesses,

Here's how to make sure you take every legal deduction that can help you lower your

income tax. You may even find that you have overpaid in a past year. If so, you can file

a refund claim on Form 843 within three years and get a refund.

In preparing your tax return, record your business income and allowable expenses on

separate Schedule C and attach it to your tax return (Form 1040). The income from Schedule

C that you show on your tax return is your net income or loss after all allowable deductions.

What You Can Deduct. Even if your outside money-making electronic

activity is mostly a hobby, you can deduct costs of any project on which you intend to

make a profit. Costs you incur for personal pleasure instead of profit are not deductible.

Keeping accurate records is the first step in cutting your income tax. You must record

daily all income received and all expenses paid. The simplest way to keep complete records

is to buy a bound journal and record your income in one part of the book and your expenses

in another. You must be able to list separately at year end your costs for (1) labor,

(2) material and supplies, (3) depreciation, (4) repairs, and (5) miscellaneous business

expenses.

Always get and keep receipts for money spent. An itemized sales slip listing the materials

or equipment bought, date, and purchase price is best.

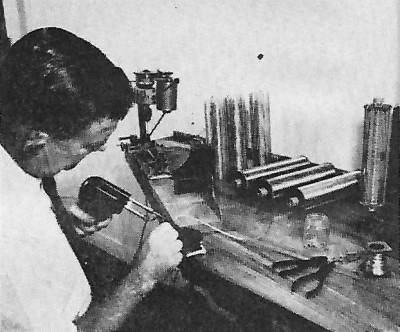

Every month Jack Falloure, owner of the J.W. Falloure Co., Houston,

Texas, ships 20 to 30 ham radio loading coils. They are made in his basement shop.

How to Handle Depreciation. Deductions for equipment depreciation

can reduce your income tax payment. You can depreciate equipment used only for business

purpose; at the rate described below. However, you must depreciate equipment used for

both hobby and business purposes according to the percentage of business use.

You must show what percentage of time your equipment is used for business by keeping

records of the number of hours the equipment is used for hobby and business purposes.

For example, if you use your test equipment 200 hours during the year and 150 of these

hours are for personal hobby use, you could deduct only 25% of the depreciation rate.

You would then use the same depreciation rate on all your test equipment unless you can

prove that the percentage of business use for part of your equipment is considerably

more than for other equipment.

Depreciation Methods Allowed. This yearly deduction can be figured

by several methods, but the simplest, most popular one is the straight-line method. Using

it, you deduct the cost of the equipment (less its estimated salvage value) in equal

yearly amounts during its useful life.

To illustrate, suppose you buy a new typewriter for $150 during the first 15 days

of January. Let's assume that its estimated salvage value after its ten-year service

life is 10% of cost, or $15. This means that you can deduct as depreciation 1/10 of $135

(cost less $15 salvage value) each year for ten years.

Details of other acceptable methods are supplied in the instruction booklet you get

with your income tax form.

Equipment with a useful life of less than one year can be fully deducted as a simple

business expense. The useful life of other equipment is the length of time you yourself

would use it before replacing it. Guidelines for the permissible useful lives of most

types of property are published in Revenue Procedure 6221 available from the U.S. Government

Printing Office.

Deduct depreciation only for the part of the year during which you own the equipment.

Equipment bought during the first half of a month is counted for the entire month, while

equipment bought during the last half of the month would be counted for the next month.

Allow 1/12 of a year's depreciation for each month you own equipment.

You can also take an "additional first-year depreciation" of 20% of the cost of income-producing

equipment with a useful life of six years or longer. This additional depreciation applies

to any property or equipment other than buildings or items that become part of a building,

such as plumbing, central air conditioning, or structural components.

You can take this entire extra deduction in the year you buy equipment, regardless

of what month of the year you buy it, along with regular depreciation for the year.

Hams snap up these 75·meter loading coils at a price of $15.95 postpaid.

Due to this part-time activity, Mr. Falloure gets quite a tax advantage.

Deductible Home Expenses. As a part-time businessman, you can deduct

part of your home expenses to cover the costs of the space you use for business. The

amount of your deductible home costs depends on both the floor space or number of rooms

used for business and the percentage of your part-time work devoted to business purposes.

For example, if you set aside one room in a rented six-room house as a workroom or office,

your allowable deduction for this space will be 1/6 of your rent. If you own your home,

you may deduct 1/6 of your costs for insurance, maintenance, taxes, and the mortgage

payment on your house (if any). Treat your costs for lights, heat, water, and telephone

in the same way, whether you rent or own your home.

If all of your part-time activity is income-producing, you can deduct the full 1/6

of your utility costs and your rent or home ownership costs. If you use the space for

both hobby and business purposes, deduct the same percentage you applied on equipment

depreciation.

Deducting Transportation Costs. Your business costs for travel or

local transportation are also deductible. The simplest way to handle them is to list

each trip in your daily expense record, giving the miles traveled and the cost. If you

pay transportation fares, list actual costs. If you drive your own car, you may deduct

either a flat rate per mile (ten cents per mile for the first 15,000 miles and seven

cents per mile after that), or record all automobile costs (including depreciation) for

the year and deduct the percentage of these costs incurred for business use.

Costs of meals and lodging are deductible only when you stay away from home overnight.

Again, be sure to record the business reason for the trip, places, dates, and the amounts

you spend. And remember to get receipts.

Trips that are partly business and partly pleasure are not considered as fully allowable

business expenses. Deduct only the costs properly attributed to business. Divide your

transportation costs on the basis of the percentage of your time spent for each purpose.

Some Final Suggestions. You may need to complete a Declaration of

Estimated Tax (Form 1040-ES) and to pay self-employment tax each year. Complete instructions

on who must file this simple form and how to file it are included in your income tax

instructions.

If your spare-time business earns as much as $400, you must also file a self-employment

tax return on Form 1040.

And finally, whenever you have a question about income tax, check with your local

Internal Revenue Service office. You will find that helpful IRS agents are almost as

anxious as you are to make sure you don't overpay your income tax.

Posted March 2, 2018

|